GST on Rent of Residential Property (New Provisions under GST)

Are you residing in a rented house ?

If answer is

YES

Don’t miss this important GST updates

The government has brought new GST rules from 18th July 2022 for ‘Renting of Residential Property’. As per notifications 05/2022 (Central Tax Rate) dated 13 July 2022, ‘Service by way of renting of a residential dwelling to a registered person is also taxable.

But we need to understand the new applicability rules because this tax would not be levied in a normal system (forward charge), it will be levied on a Reverse charge Mechanism (RCM) basis

What is Reverse charge Mechanism (RCM) ?

Reverse Charge means the liability to pay tax is on the recipient of supply of goods or services instead of the supplier of such goods or services in respect of notified categories of supply.

Through 05/2022 (Central Tax Rate) dated 13 July 2022, the following entries have been newly inserted in the list of services that attract GST on RCM basis (Original Notification 13/2017)

| Sr | Category of Supply of Services | Supplier of Service | Recipient of Service |

| 5AA | Service by way of renting of residential dwelling to a registered

person. |

Any person | Any registered person |

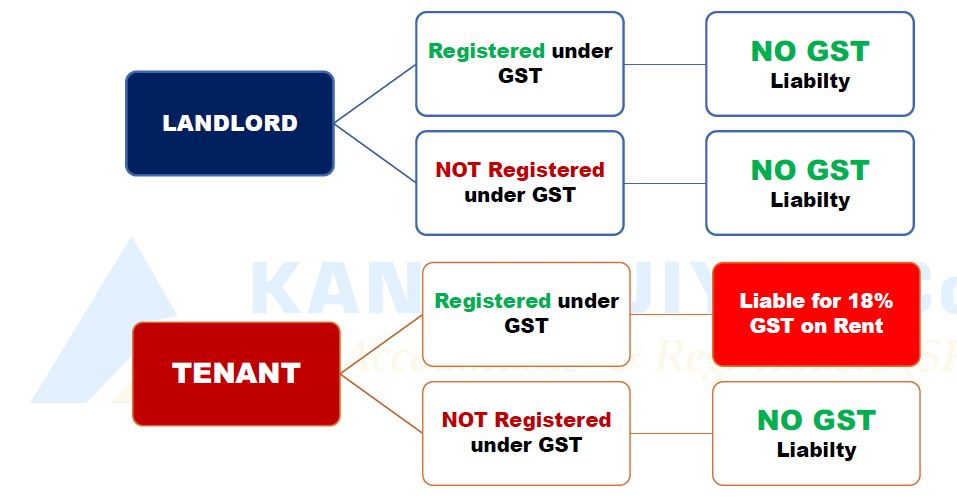

It is very clear that the conditions & responsibilities are of the tenant only. The Property Owner/landlord is not liable for any circumstance for this liability.

Thus, if you are registered under Goods & Service Tax and took a residential place on rent, then you need to pay the 18% GST on Rent from 18 July 2022.

Please note that, if the landlord/owner is registered under GST, it will not reduce/remove the liability of the tenant. Tenants have to pay compulsory the GST on a reverse charge basis

Few Important points related to the above topics

- if you running a firm/company (other than a proprietary firm) & taken GST registration, then you are not considered a registered person unless you have taken the GSTIN on your PAN.

- The purpose or use of rented premises is not relevant here, whether it is rented for business or personal GST will be levied if the above condition is satisfied.

- If you have GSTIN on your PAN and have taken the rented residential premises, please check the name in the rent agreement and discharge the tax accordingly.

Click on below file to download the the article in PDF

GST on Rented Residential Place 18.07.22 by PK

Jay Hind, Jay Bharat.

THANK YOU

Pankaj Kannaujiya